Example : Interrupted Time Series (InterruptedTimeSeries) with pymc models when the treatment time is unknown#

This notebook showcases a new feature of the InterruptedTimeSeries class in CausalPy : it now supports models that can infer the treatment time directly from the data.

We illustrate this using a built-in model from the CausalPy library, which only requires specifying the effect of the intervention. From this, the model estimates when the intervention likely occurred.

# Imports ...

import arviz as az

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

import causalpy as cp

%load_ext autoreload

%autoreload 2

%config InlineBackend.figure_format = 'retina'

seed = 42

Using the InterventionTimeEstimator PyMC model#

The InterventionTimeEstimator is designed to infer when an intervention likely occurred, based on the type of effect you expect it to have produced.

Instead of specifying the exact time of change, you describe the expected form of the intervention: a sudden jump (level), a gradual shift (trend), or a short-lived anomaly (impulse). Optionally, you can narrow the search by providing a plausible time window.

Under the hood, the model evaluates candidate intervention points and estimates how well each one explains the observed data through Bayesian inference. At its core, it relies on a linear regression, to which the intervention effects are added:

Also, in the next example, the intervention time will not be implicit. Instead, it is treated as a parameter to be inferred within a plausible window. The model then learns which value of \(t\) within this range best explains the observed data :

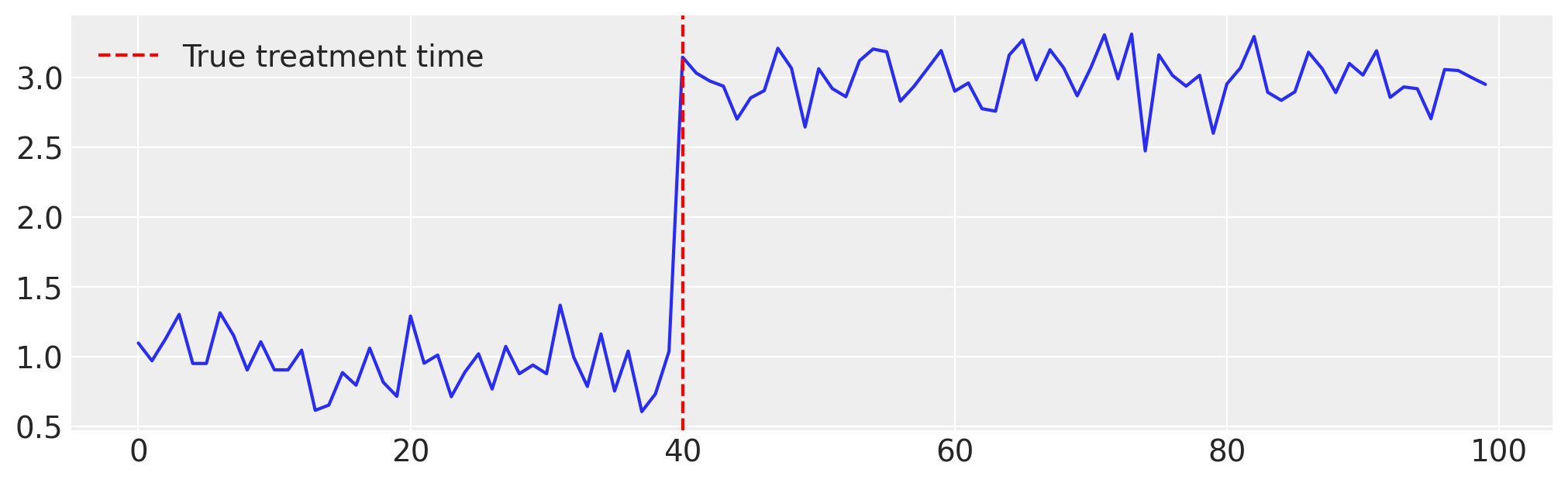

Example 1: Level Change#

In this example, we apply the InterventionTimeEstimator model to an Interrupted Time Series in its simplest form: a level change.

A level change corresponds to a sudden shift in the mean level of the series, occurring at the time of the intervention. In this case, the model can be expressed as:

where \(\sigma(t) = \frac{1}{1 + e^{-t}}\) is the logistic sigmoid function that encodes the timing of the intervention.

# Generate the Data ...

np.random.seed(seed)

n = 100

tau_true = 40

x = np.arange(n)

y = np.where(x >= tau_true, 2, 0.0) + np.random.normal(1, 0.2, size=n)

df = pd.DataFrame({"t": x, "y": y})

plt.figure(figsize=(10, 3))

plt.plot(x, y)

plt.axvline(tau_true, color="red", linestyle="--", label="True treatment time")

plt.legend();

Now, when initializing the InterventionTimeEstimator model, we only need to Ensure that InterruptedTimeSeries treatment_effect_type includes the key "level". After that, the model can be used as is with the InterruptedTimeSeries class by setting the treatment_time parameter to None.

from causalpy.experiments.interrupted_time_series import InterruptedTimeSeries

from causalpy.pymc_models import InterventionTimeEstimator

model = InterventionTimeEstimator(

treatment_effect_type="level",

)

result = InterruptedTimeSeries(

data=df,

treatment_time=None,

formula="y ~ 1 + t",

model=model,

)

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (4 chains in 4 jobs)

NUTS: [treatment_time, beta, level, sigma, y_hat]

Sampling 4 chains for 1_000 tune and 1_000 draw iterations (4_000 + 4_000 draws total) took 48 seconds.

Sampling: [beta, level, sigma, treatment_time, y_hat, y_ts]

Sampling: [y_ts]

Sampling: [y_hat, y_ts]

Sampling: [y_hat, y_ts]

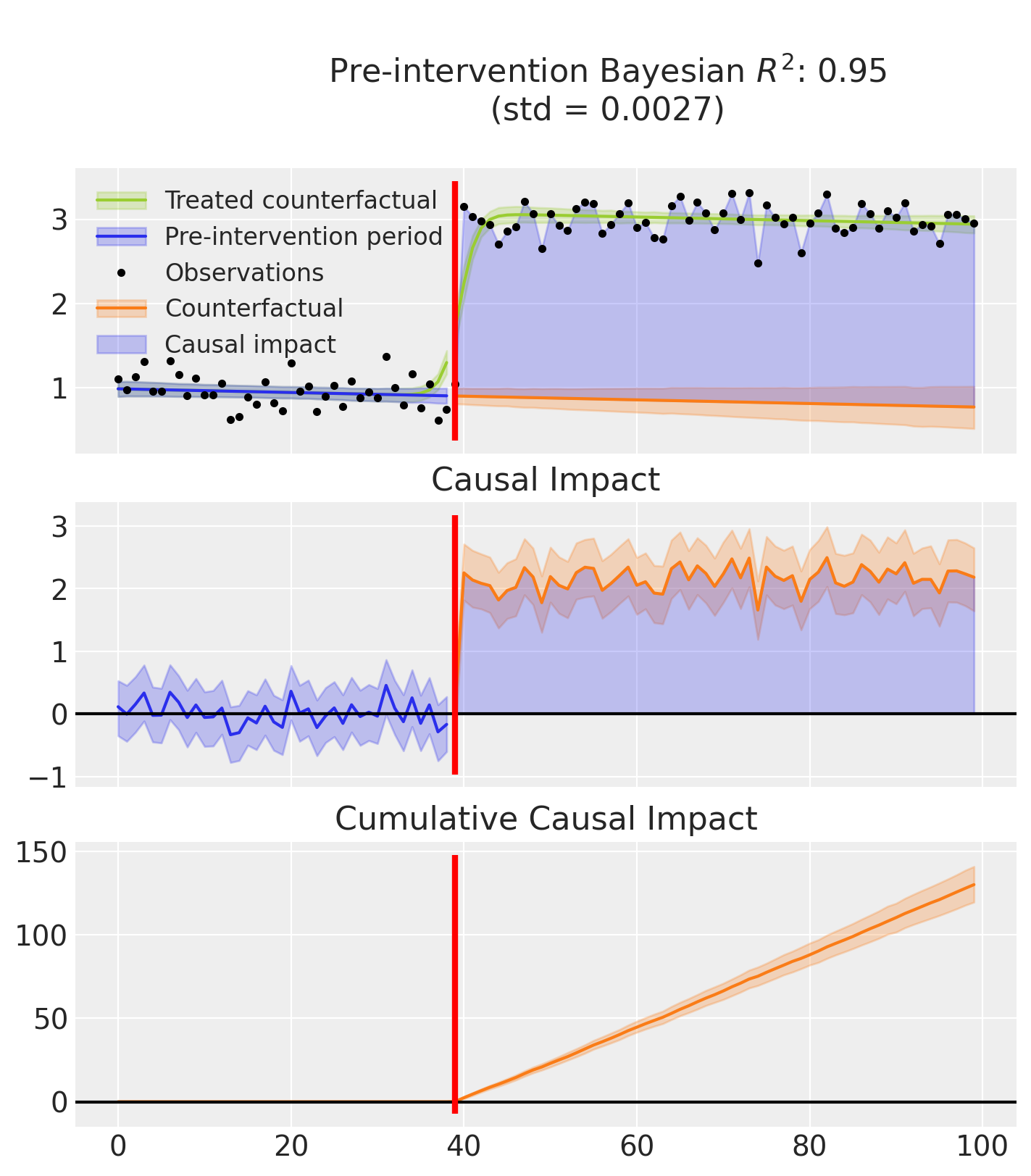

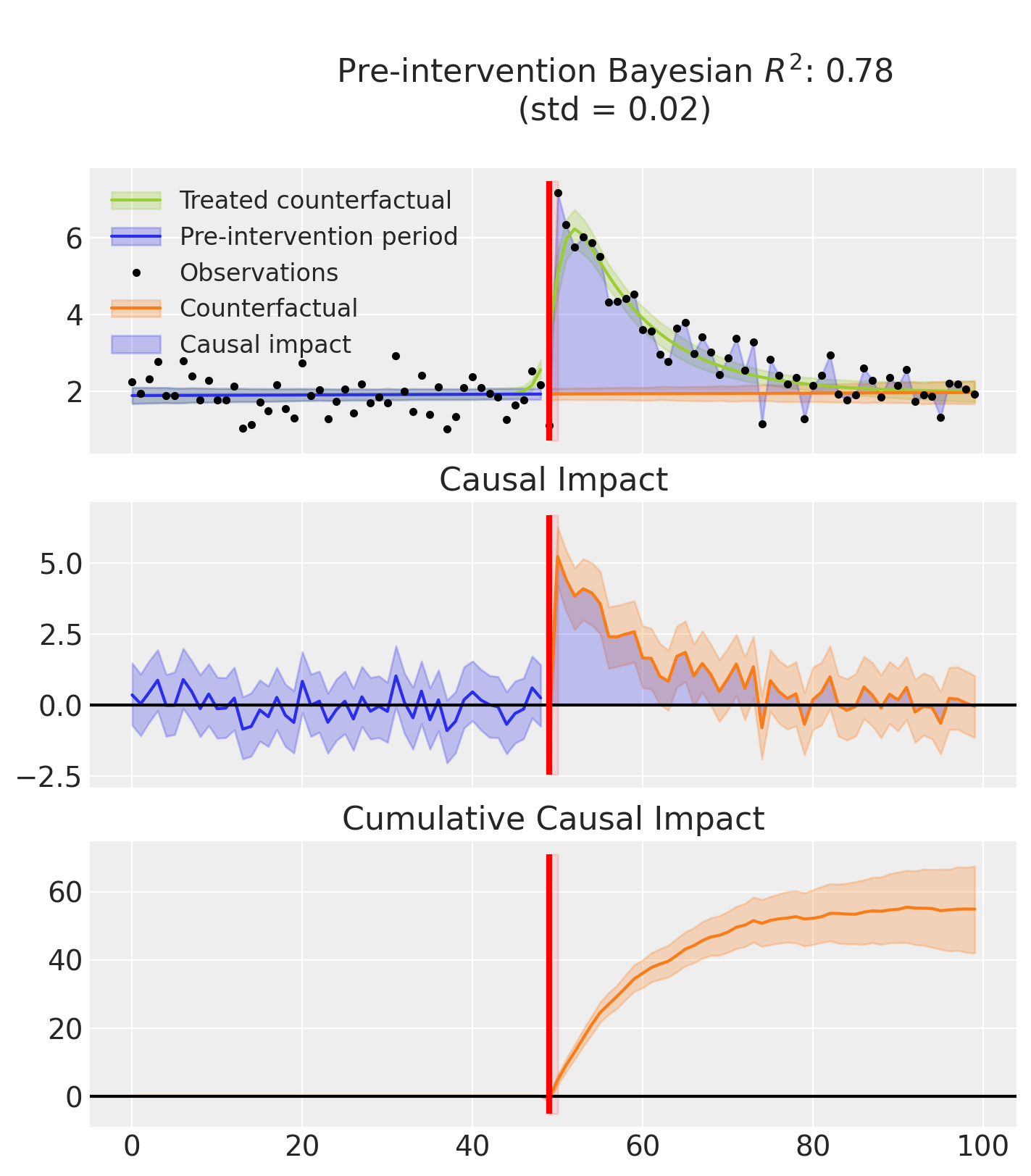

Finally, this example produces two plots.

The first displays three graphs:

the model’s predictions, showing both the fitted curve with and without the inferred causal effect,

the estimated causal impact which isolates the effect by removing it from the predictions,

and the cumulative impact over time.

The second plot shows the posterior distribution of the inferred treatment time.

Note

that the R² score is computed using the full predictions, that is, including the causal effect. In contrast, the causal impact is calculated by subtracting the estimated effect from the predictions.:::

result.plot();

result.plot_treatment_time();

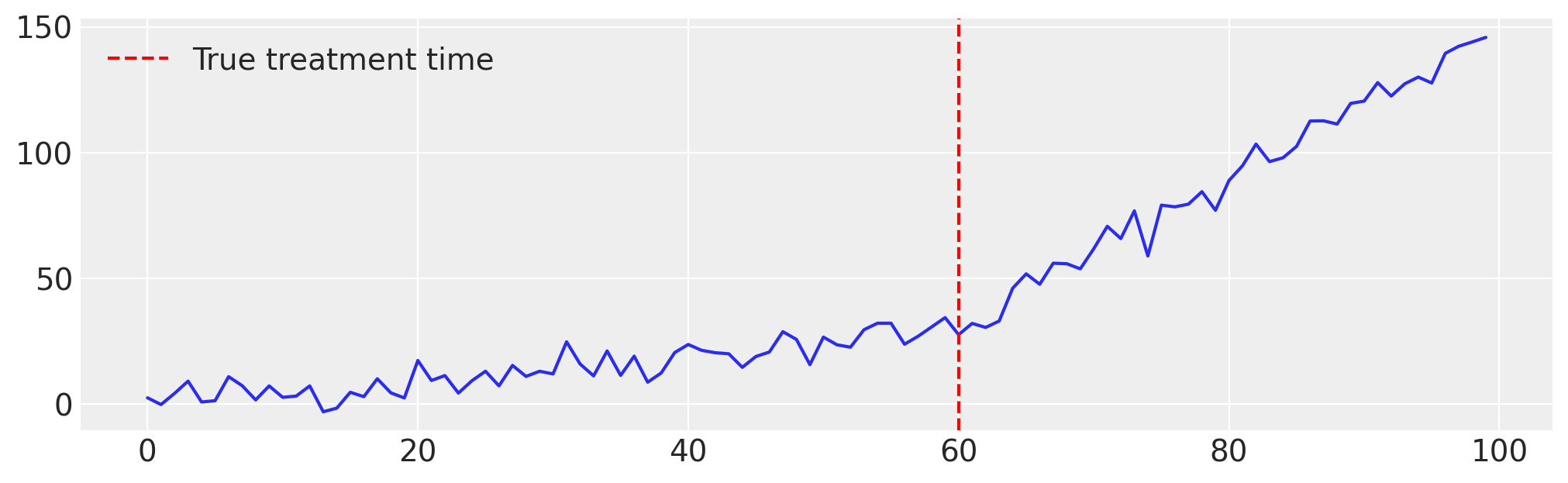

Example 2 : Trend Change#

In this example, we illustrate how to use the InterventionTimeEstimator when the time series exhibits a trend change.

A trend change corresponds to a gradual shift in the slope of the series starting at the intervention time. The model can be expressed as:

# Generate the data ...

# Set random seed for reproducibility

np.random.seed(42)

n = 100

intervention_point = 60

time = np.arange(n)

pre_trend = 0.5 * time[:intervention_point] + np.random.normal(

scale=5, size=intervention_point

)

post_trend = (

0.5 * time[intervention_point]

+ 3.0 * (time[intervention_point:] - time[intervention_point])

+ np.random.normal(scale=5, size=n - intervention_point)

)

synthetic_series = np.concatenate([pre_trend, post_trend])

# Create DataFrame

df = pd.DataFrame({"time": time, "y": synthetic_series})

# Plot

plt.figure(figsize=(10, 3))

plt.plot(df["time"], df["y"])

plt.axvline(

x=intervention_point, color="red", linestyle="--", label="True treatment time"

)

plt.legend()

plt.grid(True)

plt.show();

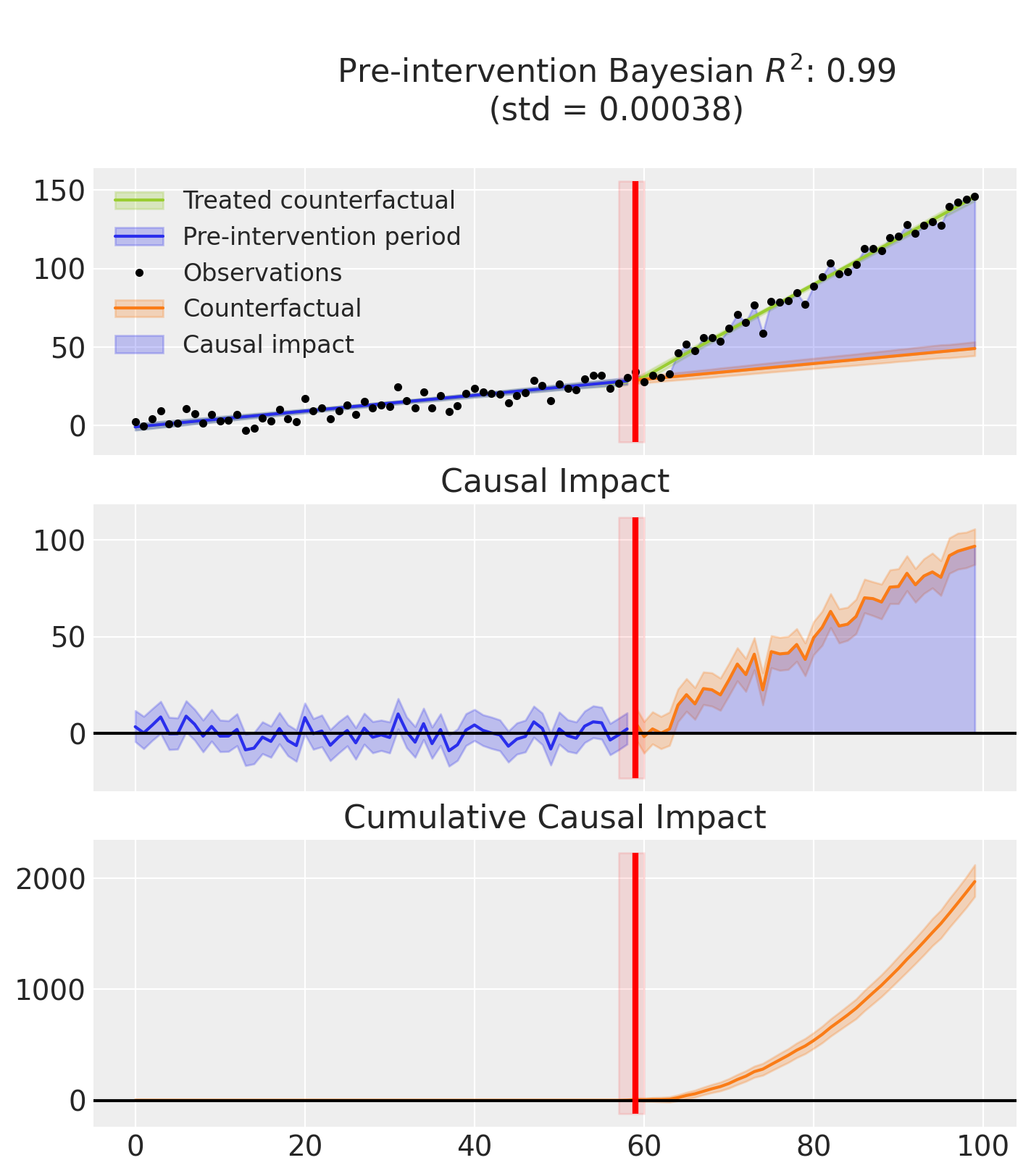

Compared to the previous example, the only change is that we use "trend" instead of "level" for the treatment_effect_type, to model a change in slope rather than a level shift.

model = InterventionTimeEstimator(

treatment_effect_type="trend",

sample_kwargs={"sample_seed": seed},

)

result = InterruptedTimeSeries(

data=df,

treatment_time=None,

formula="y ~ 1 + time",

model=model,

)

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (4 chains in 4 jobs)

NUTS: [treatment_time, beta, trend, sigma, y_hat]

Sampling 4 chains for 1_000 tune and 1_000 draw iterations (4_000 + 4_000 draws total) took 55 seconds.

Sampling: [beta, sigma, treatment_time, trend, y_hat, y_ts]

Sampling: [y_ts]

Sampling: [y_hat, y_ts]

Sampling: [y_hat, y_ts]

result.plot();

result.plot_treatment_time();

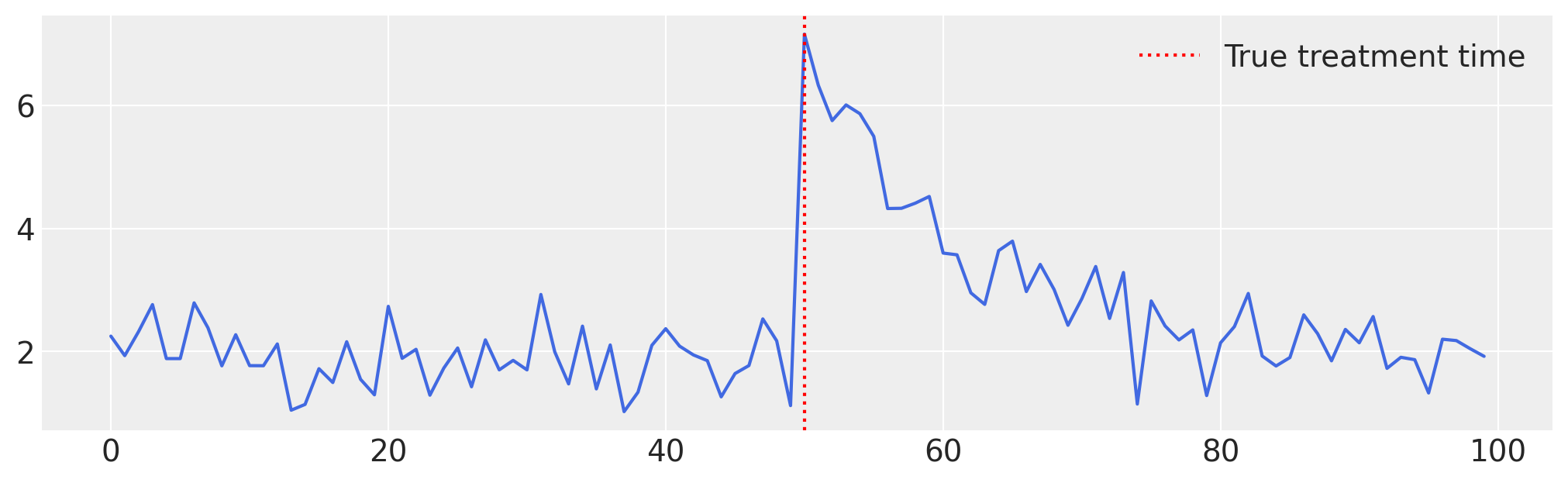

Example 3 : Impulse#

In this final example, we’ll demonstrate how to apply the InterventionTimeEstimator model to data that display an impulse-like effect. Here how it works under the hood :

# Generate data ...

np.random.seed(42)

n = 100

t = np.arange(n)

intercept = 2

trend = intercept

# Impulse parameters

t0 = 50

A = 5

decay_rate = 0.1

impulse = np.zeros(n)

impulse[t0:] = A * np.exp(-decay_rate * (t[t0:] - t0))

# Bruit

noise = np.random.normal(0, 0.5, size=n)

# Série finale

y = trend + impulse + noise

df = pd.DataFrame({"y": y, "time": t})

# Plot ...

plt.figure(figsize=(10, 3))

plt.plot(t, y, color="royalblue")

plt.axvline(t0, color="red", linestyle=":", label="True treatment time")

plt.legend()

plt.grid(True)

plt.show();

Remember to set treatment_effect_type to "impulse".

model = InterventionTimeEstimator(

treatment_effect_type="impulse",

sample_kwargs={"sample_seed": seed},

)

result = InterruptedTimeSeries(

data=df,

treatment_time=None,

formula="y ~ 1 + time",

model=model,

)

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (4 chains in 4 jobs)

NUTS: [treatment_time, beta, impulse_amplitude, decay_rate, sigma, y_hat]

Sampling 4 chains for 1_000 tune and 1_000 draw iterations (4_000 + 4_000 draws total) took 65 seconds.

Sampling: [beta, decay_rate, impulse_amplitude, sigma, treatment_time, y_hat, y_ts]

Sampling: [y_ts]

Sampling: [y_hat, y_ts]

Sampling: [y_hat, y_ts]

result.plot();

result.plot_treatment_time()

Narrowing the Inference Window#

Instead of specifying a treatment_time, you can constrain the inference window by passing a time_range=(start, end) argument, where start and end correspond to the row indices or timestamps of your dataframe:

time_range=(80,100)

or

time_range=(pd.to_datetime("2016-01-31"),pd.to_datetime("2018-01-31"))

This can significantly improve inference speed and robustness, especially when dealing with long or noisy time series.

Tip

If you’re unsure about the intervention period, try starting with time_range=None and inspect the posterior.

Keeping the same example, if we now increase the noise in the data and reduce the level change, the advantage of using a restricted time_range becomes evident:

# Making the example

n = 100

tau_true = 40

x = np.arange(n)

y = np.where(x >= tau_true, 1.60, 0.0) + np.random.normal(1, 1.21, size=n)

df = pd.DataFrame({"t": x, "y": y})

# First run: unconstrained treatment time — the model scans the entire time axis.

# With noisy data, this leads to a wide posterior and uncertain inference.

model1 = InterventionTimeEstimator(

treatment_effect_type="level",

sample_kwargs={"sample_seed": seed, "progressbar": False},

)

result1 = InterruptedTimeSeries(

data=df,

treatment_time=None,

formula="y ~ 1 + t",

model=model1,

)

# Second run: constrain the treatment time to a plausible window (t in [20, 60]).

# This narrows the posterior, improves inference stability, and speeds up sampling.

model2 = InterventionTimeEstimator(

treatment_effect_type="level",

sample_kwargs={"sample_seed": seed, "progressbar": False},

)

result2 = InterruptedTimeSeries(

data=df,

treatment_time=(20, 60),

formula="y ~ 1 + t",

model=model2,

)

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (4 chains in 4 jobs)

NUTS: [treatment_time, beta, level, sigma, y_hat]

Sampling 4 chains for 1_000 tune and 1_000 draw iterations (4_000 + 4_000 draws total) took 45 seconds.

The rhat statistic is larger than 1.01 for some parameters. This indicates problems during sampling. See https://arxiv.org/abs/1903.08008 for details

The effective sample size per chain is smaller than 100 for some parameters. A higher number is needed for reliable rhat and ess computation. See https://arxiv.org/abs/1903.08008 for details

Sampling: [beta, level, sigma, treatment_time, y_hat, y_ts]

Sampling: [y_ts]

Sampling: [y_hat, y_ts]

Sampling: [y_hat, y_ts]

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (4 chains in 4 jobs)

NUTS: [treatment_time, beta, level, sigma, y_hat]

Sampling 4 chains for 1_000 tune and 1_000 draw iterations (4_000 + 4_000 draws total) took 46 seconds.

The rhat statistic is larger than 1.01 for some parameters. This indicates problems during sampling. See https://arxiv.org/abs/1903.08008 for details

The effective sample size per chain is smaller than 100 for some parameters. A higher number is needed for reliable rhat and ess computation. See https://arxiv.org/abs/1903.08008 for details

Sampling: [beta, level, sigma, treatment_time, y_hat, y_ts]

Sampling: [y_ts]

Sampling: [y_hat, y_ts]

Sampling: [y_hat, y_ts]

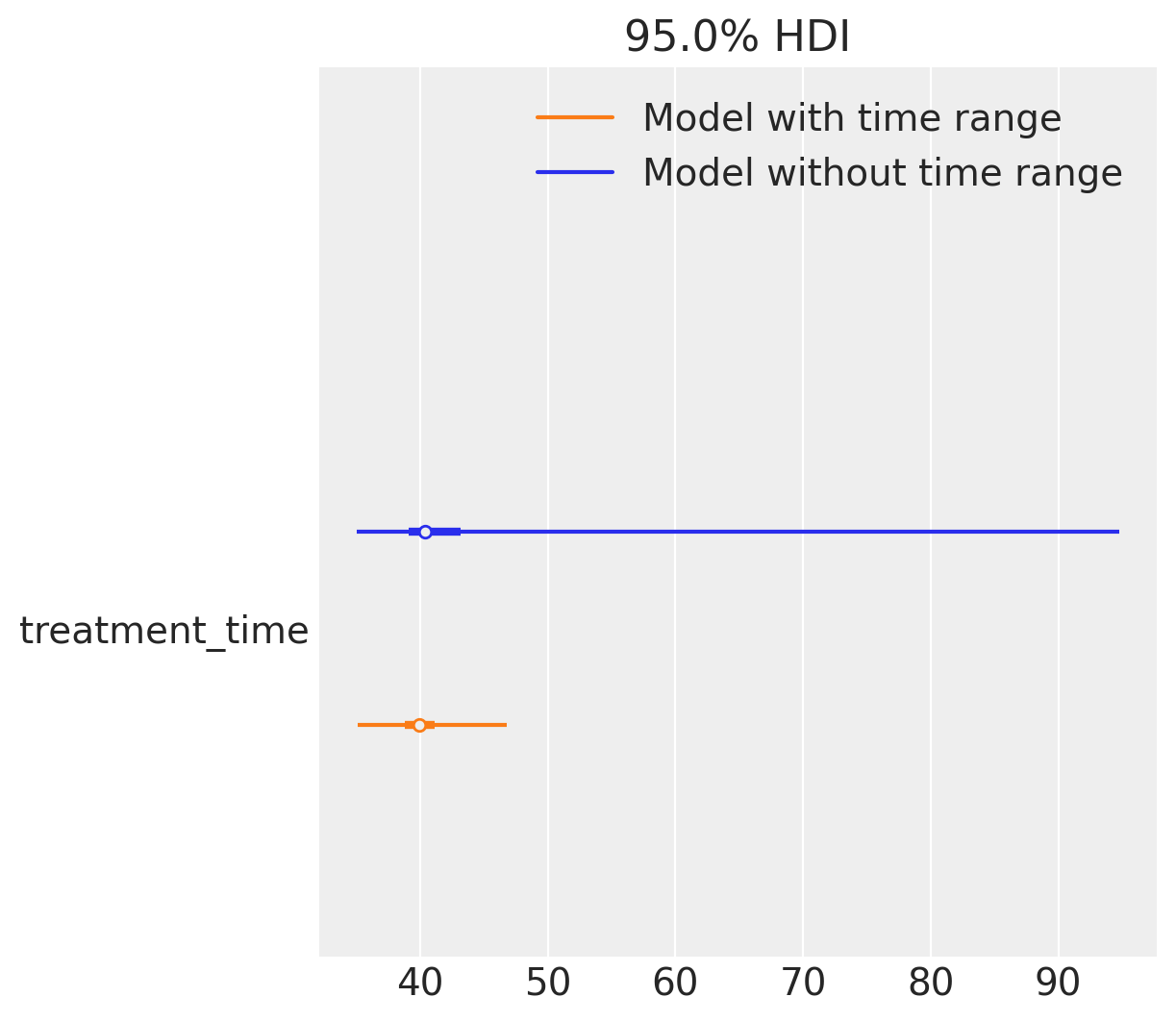

Now that we’ve increased the noise, we can already observe issues with sampling. The warning “The rhat statistic is larger than 1.01 for some parameters” indicates convergence problems: the model struggles to infer from the data, and the parameters fail to stabilize around their true values. In contrast, the model with a fixed time range does not trigger such warnings.

Looking at the forest plot, the difference becomes even clearer. The model with a given time range not only recovers the true treatment time more reliably, but it also does so with substantially less uncertainty. While the unconstrained model isn’t even centered near the correct value, its wide intervals and convergence issues mean that we cannot trust its estimates.

az.plot_forest(

[result1.idata, result2.idata],

var_names=["treatment_time"],

model_names=["Model without time range", "Model with time range"],

combined=True,

hdi_prob=0.95,

);

Specifying the effect#

The effects also can be specified using a dictionary passed to the treatment_effect_param arguments :

model = InterventionTimeEstimator(

treatment_effect_type=["level", "impulse"],

treatment_effect_param={"impulse":[mu, sigma1, sigma2]}

)

Note

You must provide all parameters if you choose to set them manually. If you leave the list empty or not fully furnished, default priors will be used.

Effect type |

Description |

Parameters required |

|---|---|---|

|

Permanent jump in the time series level |

|

|

Change in the trend slope |

|

|

Sudden change with decay |

|

Summary: How to use InterventionTimeEstimator#

Specify the time variable

Indicate which variable in the formula represents time using the time_variable_name argument.

Select the intervention effect type

Choose the expected effect(s) of the intervention: “impulse”, “level”, or “trend”.

Configure priors for each effect

Either:

use default priors or

specify custom priors (e.g.

treatment_effect_param={"impulse": [mu, sigma1, sigma2]}).

(Optional) Limit the inference window

Use

time_range=(start, end)to restrict inference to a specific time interval.Pass the model to InterruptedTimeSeries

Interrupted Time Series (InterruptedTimeSeries) : Real Data Example#

# Load Data ...

df = (

cp.load_data("covid")

.assign(date=lambda x: pd.to_datetime(x["date"]))

.set_index("date")

)

df.head()

| temp | deaths | year | month | t | pre | |

|---|---|---|---|---|---|---|

| date | ||||||

| 2006-01-01 | 3.8 | 49124 | 2006 | 1 | 0 | True |

| 2006-02-01 | 3.4 | 42664 | 2006 | 2 | 1 | True |

| 2006-03-01 | 3.9 | 49207 | 2006 | 3 | 2 | True |

| 2006-04-01 | 7.4 | 40645 | 2006 | 4 | 3 | True |

| 2006-05-01 | 10.7 | 42425 | 2006 | 5 | 4 | True |

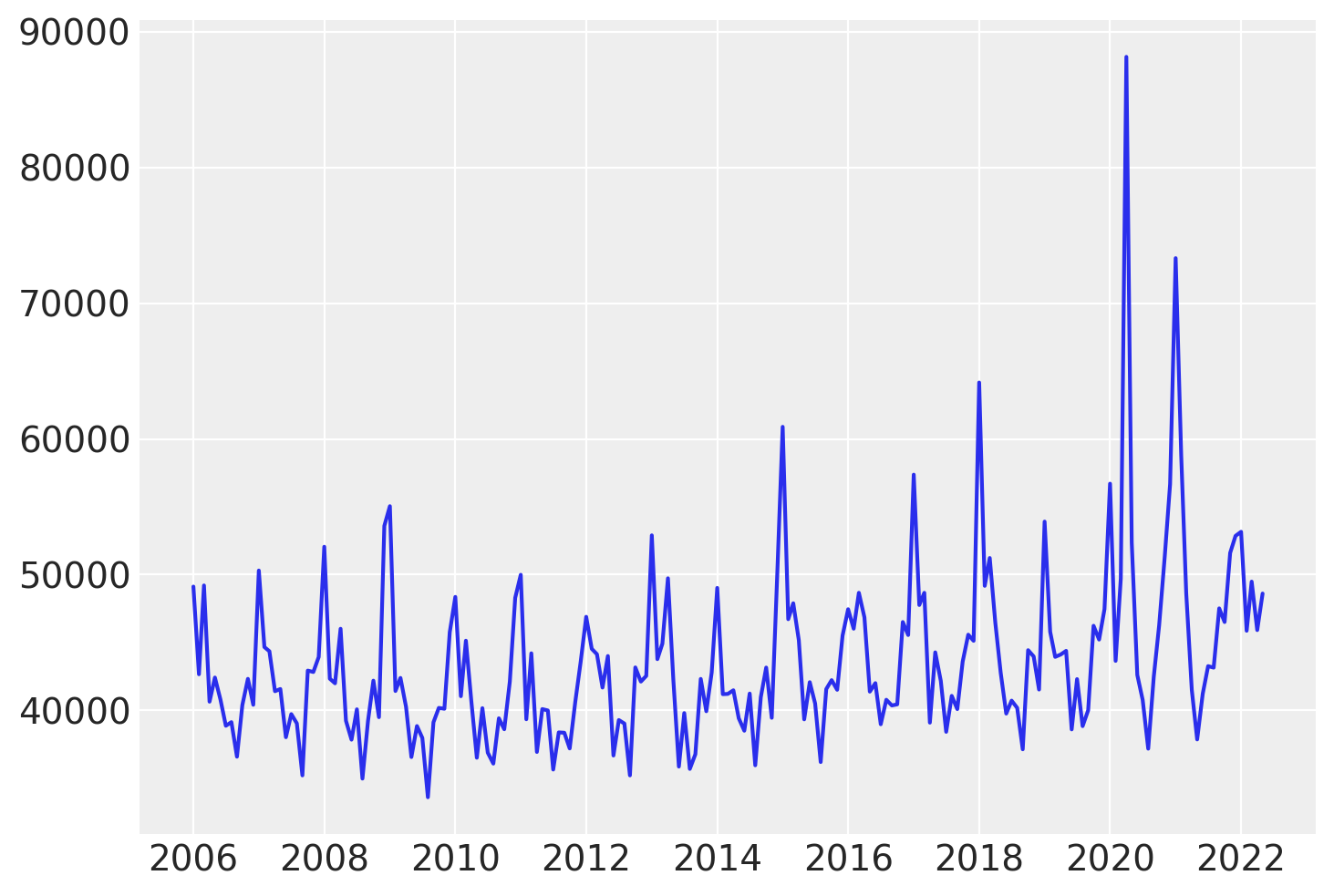

# Visualize the data ...

plt.plot(df.index, df["deaths"]);

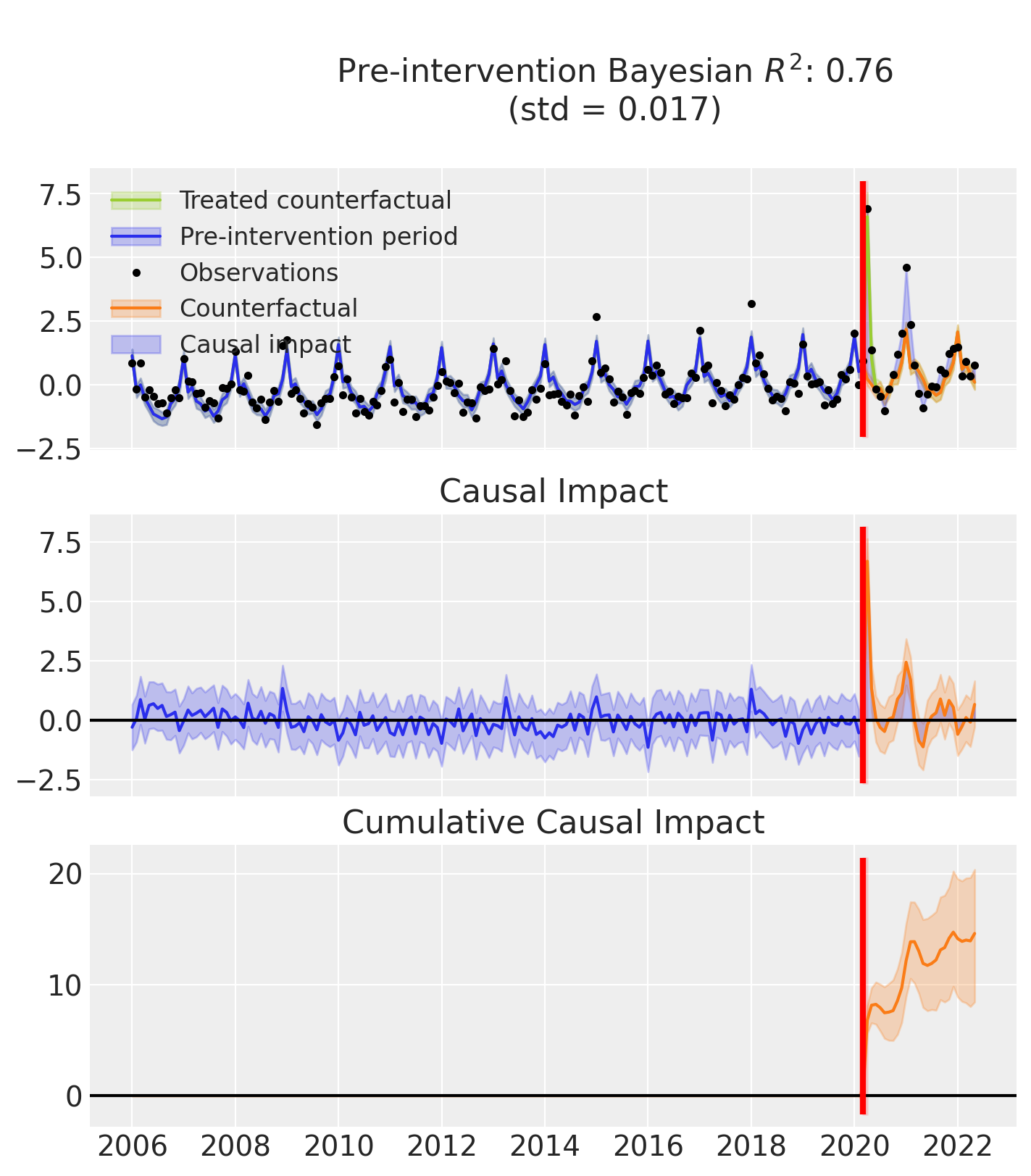

Looking at the data, we observe a noticeable increase in the number of deaths between years 2017 and 2019. After this period, the values seem to return to their previous level.

In this example, we will build a model using the “impulse” effect to represent this transient deviation. We won’t specify the exact location of the intervention, instead we will give a time range and hope the model will infer it from the data.

from causalpy.pymc_models import InterventionTimeEstimator as InterventionTimeEstimator

model = InterventionTimeEstimator(

treatment_effect_type="impulse",

sample_kwargs={"random_seed": seed, "target_accept": 0.95},

)

Run the analysis

Optionally, instead of providing a fixed treatment_time, we can guide the inference by specifying a time_range as a tuple, for example, restricting the intervention to occur between years 2014 and 2022. Leaving treatment_time=None allows the model to search freely over all possible timestamps, but adding a constraint typically speeds up inference and focuses the posterior on plausible regions.

Note

The random_seed keyword argument for the PyMC sampler is not necessary. We use it here so that the results are reproducible.

result = InterruptedTimeSeries(

df,

treatment_time=(pd.to_datetime("2014-01-01"), pd.to_datetime("2022-01-01")),

formula="standardize(deaths) ~ 0 + t + C(month) + standardize(temp)",

model=model,

)

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (4 chains in 4 jobs)

NUTS: [treatment_time, beta, impulse_amplitude, decay_rate, sigma, y_hat]

Sampling 4 chains for 1_000 tune and 1_000 draw iterations (4_000 + 4_000 draws total) took 93 seconds.

Sampling: [beta, decay_rate, impulse_amplitude, sigma, treatment_time, y_hat, y_ts]

Sampling: [y_ts]

Sampling: [y_hat, y_ts]

Sampling: [y_hat, y_ts]

Plot the results

Note

The model estimates the latent time series mu_hat by combining two components:

mu: the part inferred from the user-defined formula (e.g. time + month),mu_in: the contribution from the intervention effect.

In the plots, we display only mu — the baseline prediction based on the formula — to better highlight the causal impact of the intervention. This makes it easier to see how the observed data diverge from what would be expected without the effect.

In contrast, evaluation metrics like R² and standard deviation are computed using mu_hat, which includes both the formula and the intervention effect.

As a result, R² may appear higher than what the plots suggest.

fig, ax = result.plot()

result.plot_treatment_time();

result.summary()

==================================Pre-Post Fit==================================

Formula: standardize(deaths) ~ 0 + t + C(month) + standardize(temp)

Model coefficients:

C(month)[1] 0.8, 94% HDI [0.39, 1.2]

C(month)[2] -0.61, 94% HDI [-1, -0.22]

C(month)[3] -0.35, 94% HDI [-0.68, -0.016]

C(month)[4] -0.64, 94% HDI [-0.92, -0.37]

C(month)[5] -0.73, 94% HDI [-1, -0.45]

C(month)[6] -0.81, 94% HDI [-1.2, -0.45]

C(month)[7] -0.69, 94% HDI [-1.2, -0.23]

C(month)[8] -0.98, 94% HDI [-1.4, -0.56]

C(month)[9] -0.9, 94% HDI [-1.3, -0.53]

C(month)[10] -0.62, 94% HDI [-0.88, -0.35]

C(month)[11] -0.72, 94% HDI [-1, -0.4]

C(month)[12] -0.36, 94% HDI [-0.75, 0.026]

t 0.0051, 94% HDI [0.0039, 0.0064]

standardize(temp) -0.28, 94% HDI [-0.53, -0.027]

sigma 0.5, 94% HDI [0.46, 0.55]

As well as the model coefficients, we might be interested in the average causal impact and average cumulative causal impact.

Note

Better output for the summary statistics are in progress!

First we ask for summary statistics of the causal impact over the entire post-intervention period.

az.summary(result.post_impact.mean("obs_ind"))

| mean | sd | hdi_3% | hdi_97% | mcse_mean | mcse_sd | ess_bulk | ess_tail | r_hat | |

|---|---|---|---|---|---|---|---|---|---|

| x[unit_0] | 0.544 | 0.118 | 0.323 | 0.766 | 0.002 | 0.001 | 3397.0 | 3647.0 | 1.0 |

Warning

Care must be taken with the mean impact statistic. It only makes sense to use this statistic if it looks like the intervention had a lasting (and roughly constant) effect on the outcome variable. If the effect is transient, then clearly there will be a lot of post-intervention period where the impact of the intervention has ‘worn off’. If so, then it will be hard to interpret the mean impacts real meaning.

We can also ask for the summary statistics of the cumulative causal impact.

# get index of the final time point

index = result.post_impact_cumulative.obs_ind.max()

# grab the posterior distribution of the cumulative impact at this final time point

last_cumulative_estimate = result.post_impact_cumulative.sel({"obs_ind": index})

# get summary stats

az.summary(last_cumulative_estimate)

| mean | sd | hdi_3% | hdi_97% | mcse_mean | mcse_sd | ess_bulk | ess_tail | r_hat | |

|---|---|---|---|---|---|---|---|---|---|

| x[unit_0] | 14.606 | 3.162 | 8.436 | 20.366 | 0.054 | 0.038 | 3475.0 | 3651.0 | 1.0 |

References#

Kay H. Brodersen. Fabian Gallusser. Jim Koehler. Nicolas Remy. Steven L. Scott. “Inferring causal impact using Bayesian structural time-series models.” Ann. Appl. Stat. 9 (1) 247 - 274, March 2015. https://doi.org/10.1214/14-AOAS788

Davis Berlind, Lorenzo Cappello, Oscar Hernan Madrid Padilla. “A Bayesian framework for change-point detection with uncertainty quantification”, https://doi.org/10.48550/arXiv.2507.01558